As we kick off 2026, the clean energy landscape is heating up—literally. The National Renewable Energy Laboratory (NREL) just dropped their 2025 U.S. Geothermal Market Report, and it’s packed with data confirming what we’ve been seeing on the ground: geothermal energy has one of the strongest long-term runways in renewables. But success hinges on smart project structuring from day one.

If you’re an owner eyeing ROI, a developer scouting sites, or an engineer tackling tech challenges, this report is a must-read. We’ll break down the highlights, share practical takeaways, and tie it back to real-world execution. Let’s dive in.

The Big Picture: Steady Growth with Massive Potential

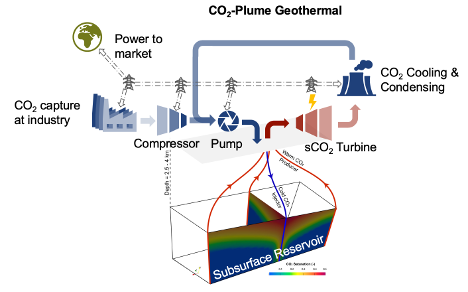

The report updates the 2021 edition and shows the U.S. geothermal sector is on a solid upward trajectory. Installed power capacity hit 3.969 GWe (gigawatts electric) by 2024, an 8% jump from 3.673 GWe in 2020. That’s a net addition of 246 MWe over four years, thanks to nine new plants and expansions like Ormat’s Mammoth GI Repowering (44.4 MWe) and Fervo’s innovative EGS pilots.

But the real excitement? Projections point to explosive scaling. Under aggressive scenarios, we could see 8-10 GW by 2030 and up to 90 GW by 2050—potentially powering 8.5% of U.S. electricity. Enhanced Geothermal Systems (EGS) are key, with domestic potential estimated at 27-57 TWe (terawatts electric). Investments are pouring in: over $1.5 billion since 2021, including $990 million in private capital for EGS.

Geothermal heat pumps (GHPs) are also booming, with 1.27 million residential units installed nationwide—highest in states like Florida and North Carolina. Mass adoption could slash grid costs by $306-606 billion by 2050, reducing summer peaks by 3-28% and improving reliability.

5 Key Takeaways from the Report

Here’s what stands out for folks in the trenches:

- Incentives Are a Game-Changer: The Inflation Reduction Act (IRA) extends tax credits through 2036, with the Clean Electricity Production Credit (up to 1.5 cents/kWh with bonuses for wages, domestic manufacturing, and energy communities) and a 30% Investment Tax Credit. States are stepping up too—29 offer power incentives, 34 for GHPs. At Walker Blue, we’ve seen clients cut costs by 20-30% by integrating these early.

- Tech Advancements Lower Barriers: EGS LCOE is dropping fast—to $45/MWh by 2035 under DOE’s Enhanced Geothermal Shot. CAPEX for deep EGS binary plants fell from $53,240/kW in 2021 to $19,757/kW in 2024. Innovations like Fervo’s Cape Station (aiming for 500 MWe by 2028) and closed-loop systems are expanding beyond traditional Western hotspots.

- Market Expansion Beyond Power: Direct-use applications (e.g., district heating in Massachusetts and New York pilots) and hybrids with solar or storage are gaining traction. Opportunities in data centers (multi-GW needs in Texas and Virginia) and mineral extraction (e.g., lithium from Salton Sea brines) could add billions in value.

- Challenges: Execution Over Tech: The report echoes what we see daily—growth is “constrained by execution, not technology or policy.” 48% of projects discontinue due to risks like permitting delays (7-10 years on BLM lands) and data gaps. Aging plants (43% over 30 years old) need upgrades.

- Implications for Stakeholders:

- Owners: Focus on ROI—hybrids can boost value by 10%, and incentives make projects bankable.

- Developers: Target non-traditional sites with EGS; 64 projects in development, but integrate labor and procurement early to avoid pitfalls.

- Engineers: Leverage drilling improvements (e.g., 500% faster rates at Utah FORGE) and modeling for better reservoir management.

| Key Metric | 2024 Status | 2030-2050 Projection |

| Installed Capacity | 3.969 GWe | 8-10 GW (2030); up to 90 GW (2050) |

| EGS LCOE | $90-110/MWh (binary) | $45/MWh (2035) |

| Investments | $1.5B+ since 2021 | $1T global by 2035 (IEA) |

| GHP Units | 1.27M residential | Mass adoption saves $306-606B grid costs |

What This Means for Your Projects

Geothermal’s edge? It’s baseload, reliable, and versatile—perfect for Kentucky’s energy mix, where we’re seeing interest in GHPs for commercial buildings. But as the report notes, “projects that capture the full value of available incentives are the ones that integrate engineering, procurement, labor strategy, and tax planning early.” That’s our sweet spot at Walker Blue—we’ve helped clients navigate these to deliver on-time, under-budget.

As deployment expands beyond traditional markets (e.g., into Eastern states like ours), that integration becomes even more critical. Think data centers or district systems—opportunities abound, but execution is key.

Wrapping Up: Time to Act

The 2025 NREL report confirms geothermal’s bright future, but only if we structure projects right from the start. With IRA incentives in play and tech costs plummeting, 2026 is shaping up to be a breakout year.

What’s your biggest takeaway? Are you working on a geothermal project and want to chat about applying these insights? Email us or drop a comment below. Let’s connect—happy to discuss how Walker Blue can help.

Stay tuned for more insights, and check out the full report here.